Every employer must withhold (and later deposit) income tax from wages paid to each employee using the computational procedures and tables prescribed by the IRS. To calculate the amount of income tax to withhold, the employer must have a properly completed Form W-4 (Employee’s Withholding Certificate) on file for each employee. By taking into account the information provided on the employee’s Form W-4, the employer determines the amount to withhold. Form W-4 is used only to determine the amount of income tax to withhold. It has no impact on the amount of social security or Medicare tax withheld by the employer.

An employer can request that each employee hired before 2020 submit a new Form W-4 but cannot require employees to do so. However, the employer should convey to employees that completing a new Form W-4 may ensure that their income tax withholding is more accurate based on the current tax rates and standard deductions. Withholding for employees who do not complete a 2020 Form W-4 will continue to be based on the number of withholding allowances claimed on their most recently completed Form W-4.

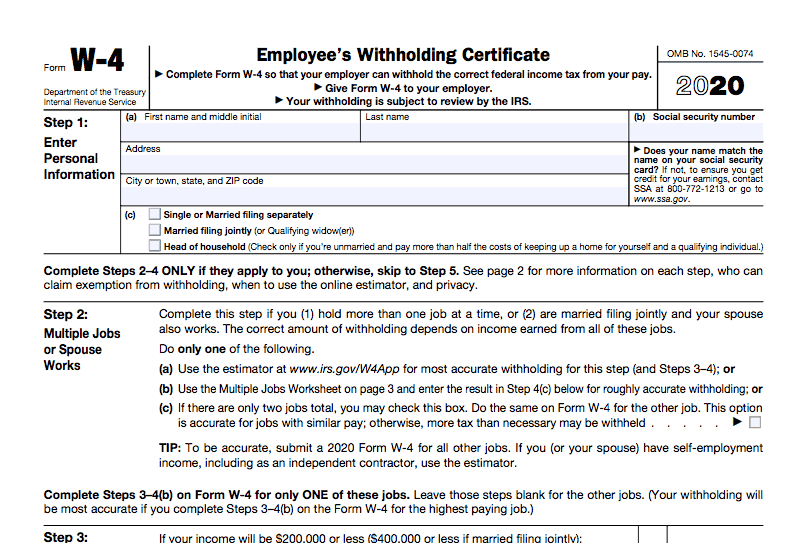

The revised 2020 Form W-4 tells the employer–

- which standard deduction and tax rates to use when determining income tax withholding based on how the employee expects to file an income tax return (single, married filing separately, married filing jointly, or as head of household),

- to withhold at a higher rate because the employee holds more than one job or the employee’s spouse also works,

- to decrease withholding because the employee will be able to claim a tax credit for one or more dependents,

- to increase withholding to account for additional income (that is not otherwise subject to withholding) or to decrease withholding to account for deductions the employee expects to claim (other than the standard deduction),

- to withhold an additional amount each pay period, and

- if the employee claims to be exempt from withholding.

Due to the substantial changes to the form, employees may be uncertain about how to complete the 2020 Form W-4. Employers should consider hosting training or educational sessions to help employees understand the methodology behind the redesigned form. However, employers must be careful to not give tax advice on the amount of the employee’s income tax withholding.

Employers may also be required to withhold state income tax. Many states rely on an employee’s Form W-4 for state income tax withholding purposes, while other states require a separate state form. States that currently rely on Form W-4, and that continue to base state income tax withholding on an individual’s number of dependents or allowances, will have to adopt changes in tax withholding calculations or issue a Form W-4 equivalent beginning in 2020. Employers should check the requirements for each state in which it has employees.